ಕನ್ನಡ ವಿಭಾಗ

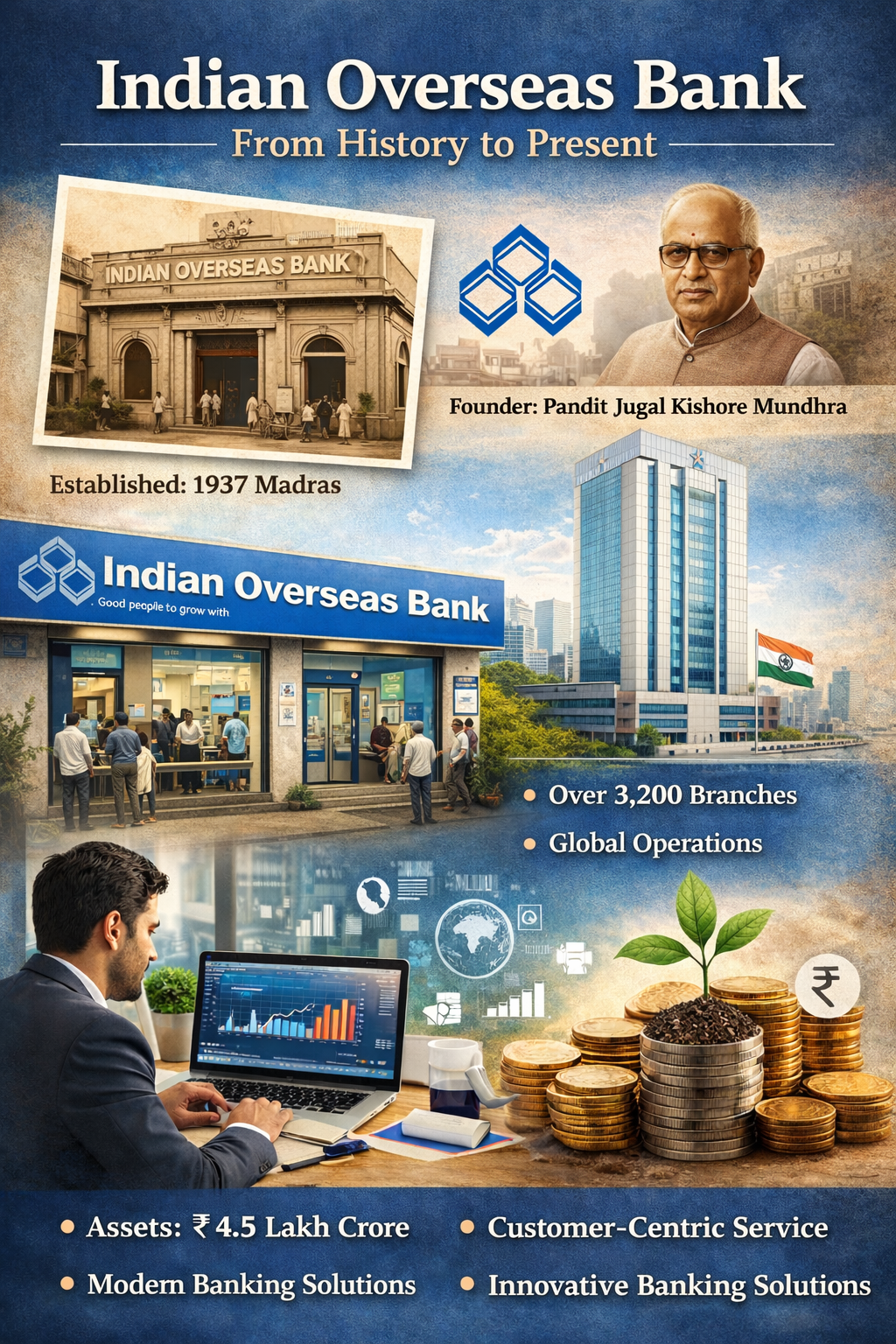

Indian Overseas Bank (IOB) ಭಾರತದಲ್ಲಿನ ಪ್ರಮುಖ ಸಾರ್ವಜನಿಕ ಕ್ಷೇತ್ರದ ಬ್ಯಾಂಕ್ಗಳಲ್ಲೊಂದು. ಈ ಬ್ಯಾಂಕ್ನ ಇತಿಹಾಸ, ಬೆಳವಣಿಗೆ, ಸೇವೆಗಳು ಮತ್ತು ಪ್ರಸ್ತುತ ಸ್ಥಿತಿಗತಿ ಬಗ್ಗೆ ತಿಳಿದುಕೊಳ್ಳುವುದು ಬ್ಯಾಂಕಿಂಗ್ ಕ್ಷೇತ್ರದ ಬಗ್ಗೆ ಆಸಕ್ತಿ ಇರುವವರಿಗೆ ಬಹಳ ಉಪಯುಕ್ತ. 1937ರಲ್ಲಿ ಚೆನ್ನೈನಲ್ಲಿ ಸ್ಥಾಪನೆಯಾದ ಈ ಬ್ಯಾಂಕ್, ಆರಂಭದಲ್ಲಿ ವಿದೇಶಿ ವ್ಯಾಪಾರ, ಎಕ್ಸ್ಚೇಂಜ್ ವ್ಯವಹಾರ ಮತ್ತು ಅಂತರರಾಷ್ಟ್ರೀಯ ಹಣಕಾಸು ಸೇವೆಗಳ ಮೇಲೆ ಹೆಚ್ಚು ಗಮನ ನೀಡಿತು. ಅದೇ ಕಾರಣಕ್ಕೆ ಇದರ ಹೆಸರಲ್ಲೇ “Overseas” ಎಂಬ ಪದ ಸೇರಿದೆ. ಸಮಯದೊಂದಿಗೆ ಇದು ಕೇವಲ ವಿದೇಶಿ ವ್ಯವಹಾರಗಳಿಗೆ ಮಾತ್ರ ಸೀಮಿತವಾಗದೆ, ಸಾಮಾನ್ಯ ಜನರಿಗೆ ಬೇಕಾದ ಎಲ್ಲ ಬ್ಯಾಂಕಿಂಗ್ ಸೇವೆಗಳನ್ನು ನೀಡುವ ದೊಡ್ಡ ಬ್ಯಾಂಕ್ ಆಗಿ ವಿಸ್ತರಿಸಿತು.

Indian Overseas Bank ಅನ್ನು ಸ್ಥಾಪಿಸಿದವರು M. Ct. M. Chidambaram Chettyar. ಅವರು ವಾಣಿಜ್ಯ, ಹಣಕಾಸು ಮತ್ತು ಕೈಗಾರಿಕಾ ಅಭಿವೃದ್ಧಿಯ ದೃಷ್ಟಿಯಿಂದ ಈ ಬ್ಯಾಂಕ್ ಅನ್ನು ಆರಂಭಿಸಿದ್ದರು. ಆರಂಭಿಕ ವರ್ಷಗಳಲ್ಲಿ ಬ್ಯಾಂಕ್ ಭಾರತದೊಳಗೆ ಮಾತ್ರವಲ್ಲದೆ ವಿದೇಶಗಳಲ್ಲೂ ತನ್ನ ಪಾದಾರ್ಪಣೆ ಮಾಡಿತು. ವಿಶೇಷವಾಗಿ ಭಾರತೀಯ ವಲಸಿಗರು, ವ್ಯಾಪಾರಿಗಳು ಮತ್ತು ಅಂತರರಾಷ್ಟ್ರೀಯ ವ್ಯವಹಾರಗಳಲ್ಲಿ ತೊಡಗಿದ್ದ ಗ್ರಾಹಕರಿಗೆ ಇದು ಉಪಯುಕ್ತವಾಗಿತ್ತು. ಭಾರತ ಸ್ವಾತಂತ್ರ್ಯ ನಂತರದ ಅವಧಿಯಲ್ಲಿ ಬ್ಯಾಂಕಿಂಗ್ ಕ್ಷೇತ್ರದಲ್ಲಿ ನಡೆದ ಬದಲಾವಣೆಗಳೊಂದಿಗೆ IOB ಕೂಡ ತನ್ನ ಕಾರ್ಯವ್ಯಾಪ್ತಿಯನ್ನು ವಿಸ್ತರಿಸಿಕೊಂಡಿತು.

1969ರಲ್ಲಿ ಬ್ಯಾಂಕ್ ರಾಷ್ಟ್ರೀಕರಣಗೊಂಡ ನಂತರ, Indian Overseas Bank ಸಾರ್ವಜನಿಕ ಕ್ಷೇತ್ರದ ಬ್ಯಾಂಕ್ ಆಗಿ ರೂಪಾಂತರಗೊಂಡಿತು. ರಾಷ್ಟ್ರೀಕರಣದ ನಂತರ ಬ್ಯಾಂಕಿಂಗ್ ಸೇವೆಗಳು ಗ್ರಾಮೀಣ ಮತ್ತು ಅರ್ಧನಗರ ಪ್ರದೇಶಗಳಿಗೂ ತಲುಪಲು ಆರಂಭವಾಯಿತು. ಖಾತೆ ತೆರೆಯುವುದು, ಉಳಿತಾಯ ಯೋಜನೆಗಳು, ಕೃಷಿ ಸಾಲ, ಶಿಕ್ಷಣ ಸಾಲ, ಗೃಹ ಸಾಲ, ವ್ಯಾಪಾರ ಸಾಲ, MSME ಬೆಂಬಲ ಮತ್ತು ಡಿಜಿಟಲ್ ಬ್ಯಾಂಕಿಂಗ್ ಸೇವೆಗಳಂತಹ ಹಲವು ಕ್ಷೇತ್ರಗಳಲ್ಲಿ ಬ್ಯಾಂಕ್ ತನ್ನ ಸೇವೆಗಳನ್ನು ಬಲಪಡಿಸಿತು. ಇದರಿಂದ ಜನಸಾಮಾನ್ಯರಿಗೆ ಹಣಕಾಸು ಸೇವೆಗಳು ಸುಲಭವಾಯಿತು.

ವರ್ತಮಾನದಲ್ಲಿ Indian Overseas Bank ತನ್ನ ಶಾಖಾ ಜಾಲ, ATM ಸೇವೆಗಳು, ಮೊಬೈಲ್ ಬ್ಯಾಂಕಿಂಗ್, ಇಂಟರ್ನೆಟ್ ಬ್ಯಾಂಕಿಂಗ್ ಮತ್ತು UPI ಮೂಲಕ ಗ್ರಾಹಕರಿಗೆ ಸುಲಭ ಸೇವೆ ನೀಡುತ್ತಿದೆ. ಇಂದಿನ ಡಿಜಿಟಲ್ ಯುಗದಲ್ಲಿ ಗ್ರಾಹಕರು ವೇಗವಾದ ಮತ್ತು ಸುರಕ್ಷಿತ ಬ್ಯಾಂಕಿಂಗ್ ನಿರೀಕ್ಷಿಸುತ್ತಾರೆ. ಈ ಅಗತ್ಯಕ್ಕೆ ಹೊಂದಿಕೊಳ್ಳಲು ಬ್ಯಾಂಕ್ ತನ್ನ ತಂತ್ರಜ್ಞಾನ ವ್ಯವಸ್ಥೆಗಳನ್ನು ನಿರಂತರವಾಗಿ ನವೀಕರಿಸುತ್ತಿದೆ. ಯುವ ಗ್ರಾಹಕರು, ವೇತನ ಖಾತೆದಾರರು, ಉದ್ಯಮಿಗಳು ಮತ್ತು ಹಿರಿಯ ನಾಗರಿಕರು ಎಲ್ಲರಿಗೂ ತಕ್ಕಂತೆ ವಿವಿಧ ಉತ್ಪನ್ನಗಳನ್ನು ಬ್ಯಾಂಕ್ ನೀಡುತ್ತಿದೆ.

ಬ್ಯಾಂಕಿನ ಮತ್ತೊಂದು ಪ್ರಮುಖ ಬಲ ಅಂಶವೆಂದರೆ ಅದರ ಸಾರ್ವಜನಿಕ ವಿಶ್ವಾಸ. ದೀರ್ಘ ಇತಿಹಾಸ, ಸರ್ಕಾರದ ಬೆಂಬಲ ಮತ್ತು ರಾಷ್ಟ್ರವ್ಯಾಪಿ ಸೇವೆಗಳ ಕಾರಣದಿಂದ IOB ಇನ್ನೂ ಅನೇಕ ಗ್ರಾಹಕರಿಗೆ ವಿಶ್ವಾಸಾರ್ಹ ಆಯ್ಕೆಯಾಗಿದೆ. ಜೊತೆಗೆ, ಬ್ಯಾಂಕ್ ತನ್ನ ಸಾಲ ಪೋರ್ಟ್ಫೋಲಿಯೊ, NPA ನಿಯಂತ್ರಣ, ಡಿಜಿಟಲ್ ಪರಿವರ್ತನೆ ಮತ್ತು ಗ್ರಾಹಕ ಅನುಭವದ ಸುಧಾರಣೆಗೆ ಒತ್ತು ನೀಡುತ್ತಿದೆ. ಈ ಕ್ರಮಗಳು ಬ್ಯಾಂಕ್ನ ದೀರ್ಘಾವಧಿ ಸ್ಥಿರತೆಗೆ ಸಹಕಾರಿಯಾಗುತ್ತವೆ.

ಬ್ಯಾಂಕಿನ ಪ್ರಸ್ತುತ ಸ್ಥಿತಿಗತಿಯನ್ನು ನೋಡಿದರೆ, Indian Overseas Bank ಒಂದು ಸ್ಥಿರವಾಗಿ ಕಾರ್ಯನಿರ್ವಹಿಸುತ್ತಿರುವ ಸಾರ್ವಜನಿಕ ವಲಯದ ಬ್ಯಾಂಕ್ ಆಗಿದೆ. ಹಲವು ಸವಾಲುಗಳಿದ್ದರೂ, ಬ್ಯಾಂಕ್ ತನ್ನ ಪುನಶ್ಚೇತನ, ತಂತ್ರಜ್ಞಾನ ಸ್ವೀಕಾರ ಮತ್ತು ಸೇವಾ ಸುಧಾರಣೆಯ ಮೂಲಕ ಮುಂದೆ ಸಾಗುತ್ತಿದೆ. ಭಾರತದ ಬ್ಯಾಂಕಿಂಗ್ ವ್ಯವಸ್ಥೆಯಲ್ಲಿ ಇದರ ಸ್ಥಾನ ಇನ್ನೂ ಮಹತ್ವದ್ದಾಗಿದೆ. ವಿಶೇಷವಾಗಿ ದಕ್ಷಿಣ ಭಾರತದಲ್ಲಿ ಇದರ ಬಲವಾದ ಹಾಜರಾತಿ ಇದೆ, ಆದರೆ ದೇಶದ ಇತರ ಭಾಗಗಳಲ್ಲಿಯೂ ಬ್ಯಾಂಕ್ ಸೇವೆಗಳು ವಿಸ್ತರಿಸಿವೆ.

ಮೋನೆಟೈಸೇಶನ್ ದೃಷ್ಟಿಯಿಂದ ಇಂತಹ ವಿಷಯಗಳು ಉತ್ತಮವಾಗಿ ಕಾರ್ಯನಿರ್ವಹಿಸುತ್ತವೆ, ಏಕೆಂದರೆ ಬ್ಯಾಂಕಿಂಗ್, ಸಾಲ, ಖಾತೆ, ಡಿಜಿಟಲ್ ಪಾವತಿ, IFSC, ಮತ್ತು ಹಣಕಾಸು ಸೇವೆಗಳ ಬಗ್ಗೆ ಜನರಲ್ಲಿ ಸದಾ ಆಸಕ್ತಿ ಇರುತ್ತದೆ. SEO ದೃಷ್ಟಿಯಿಂದ “Indian Overseas Bank history”, “Indian Overseas Bank present status”, “Indian Overseas Bank current status”, “Indian Overseas Bank in Kannada” ಎಂಬ ಕೀವರ್ಡ್ಗಳನ್ನು ಸಹಜವಾಗಿ ಬಳಸಬಹುದು. ಇದರಿಂದ ಹುಡುಕಾಟದಲ್ಲಿ ಉತ್ತಮ ಫಲಿತಾಂಶ ಸಿಗಲು ಸಾಧ್ಯ.

ಒಟ್ಟಿನಲ್ಲಿ, Indian Overseas Bank ಭಾರತೀಯ ಬ್ಯಾಂಕಿಂಗ್ ಇತಿಹಾಸದ ಒಂದು ಪ್ರಮುಖ ಭಾಗವಾಗಿದೆ. ಅದರ ಇತಿಹಾಸವು ಉದ್ಯಮಶೀಲತೆಯನ್ನು ಪ್ರತಿಬಿಂಬಿಸುತ್ತದೆ; ಅದರ ವರ್ತಮಾನವು ಡಿಜಿಟಲ್ ಯುಗದೊಂದಿಗೆ ಹೊಂದಿಕೊಳ್ಳುವ ಶಕ್ತಿಯನ್ನು ತೋರಿಸುತ್ತದೆ; ಮತ್ತು ಅದರ ಸ್ಥಿತಿಗತಿ ಮುಂದಿನ ಬೆಳವಣಿಗೆಗೆ ಇರುವ ಸಾಮರ್ಥ್ಯವನ್ನು ಸೂಚಿಸುತ್ತದೆ. ಈ ಬ್ಯಾಂಕ್ ಮುಂದೆಯೂ ಗ್ರಾಹಕರಿಗೆ ವಿಶ್ವಾಸಾರ್ಹ ಸೇವೆ ನೀಡುವ ಮೂಲಕ ತನ್ನ ಸ್ಥಾನವನ್ನು ಉಳಿಸಿಕೊಂಡಿರಲಿದೆ.

English Section

Indian Overseas Bank (IOB) is one of India’s well-known public sector banks with a long and meaningful history. Founded in 1937 in Chennai by M. Ct. M. Chidambaram Chettyar, the bank was created with a vision to support overseas trade, exchange business, and international financial services. The name “Overseas” itself reflects that early purpose. Over the years, however, the bank expanded far beyond its original focus and became a trusted financial institution serving millions of customers across India.

In its early phase, Indian Overseas Bank built a reputation among traders, business communities, and Indian customers involved in international operations. It was not just a bank for deposits and withdrawals; it was also a bridge for financial activity connected to foreign markets. After India’s independence, the banking landscape changed significantly, and IOB adapted to new priorities by expanding its domestic reach and customer services.

A major turning point came in 1969, when the bank was nationalized along with other leading banks in India. This move changed its role from a privately managed institution to a public sector bank serving broader national goals. After nationalization, Indian Overseas Bank grew its branch network and began serving urban, semi-urban, and rural customers more actively. It played an important role in supporting savings, loans, agriculture, education, housing, business development, and everyday banking needs.

Today, Indian Overseas Bank continues to operate as a public sector bank with a wide range of banking products and services. Customers can use savings accounts, current accounts, fixed deposits, retail loans, MSME financing, digital banking, mobile banking, and internet banking services. The bank has also been working to align itself with modern banking trends, where speed, convenience, and security matter more than ever.

In the present banking environment, digital transformation is essential. Indian Overseas Bank has been adapting to this shift by improving online services, UPI-based payments, and customer-facing technology. These improvements help the bank stay relevant in a market where private banks, fintech platforms, and digital-first services are growing rapidly. For many customers, especially those who prefer the trust of a government-backed bank, IOB remains a dependable choice.

The current status of Indian Overseas Bank can be described as stable, service-focused, and transformation-driven. Like many public sector banks, it has faced industry-wide challenges such as asset quality pressure, competition, and the need for modernization. Still, its long-standing presence, government support, and strong customer base give it a solid foundation. The bank continues to work on efficiency, digital adoption, and better customer experience.

From an SEO and monetization point of view, this topic is highly valuable because banking content attracts consistent search demand. Articles about bank history, current status, and digital banking often perform well with users looking for financial information, educational content, and comparison material. A clear structure, keyword-rich headings, and useful subtopics can help improve visibility and ad revenue potential.

In conclusion, Indian Overseas Bank is more than just a financial institution. It is a part of India’s banking history, a participant in the country’s digital banking transition, and a continuing public sector player with a strong legacy. Its journey from an overseas trade-focused bank to a nationwide service provider shows how Indian banking has evolved over time. The bank’s future will likely depend on how well it continues balancing trust, technology, and customer needs.